Alternative payment methods in the Travel & Hospitality industry

In the tourism and hospitality industry, companies are constantly looking for ways to enhance their customers’ experience. One of the ways in which this can be achieved is by offering a variety of payment methods, beyond traditional credit and debit cards. Alternative payment methods have emerged as a solution to provide a simpler, safer and faster payment experience for customers.

In this article, we will explain some of the alternative payment methods being used in the travel and hospitality industry: from wallets to instant transfers, BNPL and non-bank payment methods. We will discuss the pros and cons of each, how they can help companies improve their customers’ payment experience, reduce transaction costs and increase conversion rates.

Wallets

Digital wallets are simply “electronic cardholders” that securely store virtual versions of debit and credit cards. The main and best known by users are Apple Pay and Google Pay, for users of Iphone or Android phones, although there are others such as Click to Pay that are independent of the device. Wallets store card data, shipping address and other user data.

These wallets are not exclusive to online, as they share data between browsers, Safari for Apple Pay or Chrome for Google Pay. Face-to-face payments can also be made thanks to the fact that these wallets also have an app that interacts with the NFC chip of the device where they are installed. In contrast, Click 2 Pay works on any browser and is device-independent, as it does not require an app but is not used to make physical payments.

Wallets have been very popular with the public, especially with young people because they are convenient, fast and easy to use. You don’t have to enter your card details or dig through your wallet every time you want to pay. Payment information is stored in a single, centralized and secure location.

Instant Transfer

With the implementation of PSD2 and thanks to the SEPA protocol and its instant transfer between European banks, it allows third parties known as TTP, Third Party Provider, to send transaction orders from one bank to another. In the European market we can find:

Payments with Sofort

Sofort is an online payment system that allows users to make transfers directly from their bank account in real time. It is a popular payment solution in Europe and is used in a variety of sectors from e-commerce to financial services and online gaming.

Payments with iDeal

IDEAL is an online payment method used mainly in the Netherlands. Its acronym stands for “Enhanced Interactive Online Banking System” in Dutch. It is a payment service that allows customers of Dutch banks to pay online using their bank accounts. It is similar to other online payment services such as PayPal or Stripe, but is specifically designed for online banking in the Netherlands.

Payments with Giropay

Giropay is an online payment method used in Germany that allows customers to make payments via real-time bank transfers. It was launched in 2006 and is supported by most German banks. When choosing giropay as a payment method, the customer is redirected to their bank’s website to log in and authorize the transfer. Once the transfer is completed, the payment is confirmed and the seller receives a notification that the payment has been processed.

Payments with Bizum

Bizum is a mobile payment platform in Spain that allows users to send and receive money from their mobile devices quickly and easily. It is an initiative developed by a group of Spanish banks that allows users to link their cell phone numbers with their bank accounts and make instant payments through a mobile application. It currently has more than 23 million users and is an increasingly popular payment option in physical and online stores. Bizum has evolved into a payment solution for merchants and currently more than 44,000 merchants in Spain accept Bizum payments from their customers.

Payment Initiation

With the entry into force of the PSD2 regulation, in addition to the introduction of SCA (Strong Customer Authentication), it also prompted banks to develop APIs that could interact with their services; this process of innovation in the UK is known as Open Banking. Two of these APIs are Banking Aggregation and Payment Initiation, the latter allowing us to request a transfer from one bank account to another. It should be noted that this service is currently only available with European banks and for merchants with an account in a European bank.

In our case, we offer our merchants this service through PaynoPain Financial Services, our payment institution that has the Payment Institution license granted by the Bank of Spain that allows us to manage this type of transactions.

Payment Initiation or Account 2 Account services also rely on SEPA Instant Transfers, but with the difference that the payer enters his bank and authorizes the transfer, without an intermediary service such as Sofort or Bizum, this allows to order payments with larger amounts in which it is better to make the transfers from online banking.

Buy now, pay later (BNPL) or Buy now, pay later

“Buy now, pay later”, installment financing solutions have gained a lot of prominence in recent years, especially among the younger public. They are an alternative that can help businesses increase their sales because their customers can purchase products or services for higher amounts, more comfortably and without having to give up other things.

This alternative payment method is very useful for those reservations or purchases where the amount to pay is high so it can give problems with the cards or not having all that capital available, here the consumer credit option facilitates the confirmation of the purchase and helps the buyer to acquire that trip or stay you want.

Its operation is very simple: at the end of the purchase, the customer chooses the payment method “Buy now, pay later” and the installments or installments of financing, the entity that provides this service checks that the user has solvency and approves the transaction. Payments will be made automatically in the selected periods and the merchant will receive the full amount of the transaction at the time of purchase, thus securing the funds without any risk.

Alternative non-European payment methods

While traditional payment methods such as credit cards remain popular in Europe, more innovative and efficient payment systems have been developed in other parts of the world and have gained wide acceptance among consumers. Outside the Eurozone or SEPA, each country has created its own alternative payment methods that are adapted to the idiosyncrasies of each country.

We will explain the most popular payment methods according to each continent:

Payments in Asia

Payments with WeChat and AliPay

In the main Asian countries, China and India, two services known as “Super Apps” stand out: WeChat Pay and Alipay.

WeChat Pay is integrated within the popular instant messaging platform WeChat and Alipay was developed by Chinese e-commerce giant Alibaba and both offer similar services. WeChat Pay is integrated within the popular instant messaging platform WeChat and Alipay was developed by Chinese e-commerce giant Alibaba and both offer similar services. You can order a cab, shop in their marketplace, pay electricity bills, make transfers to friends, pay online or in person, book a trip, purchase credit and many other things. All of these services are built on top of a social network that offers instant messaging, photo sharing, networking and everything we know in the West as Meta services and products.

Payments in Africa

Although it is still a continent that receives more travelers than it sends out, it is important to know their preferences as well. In general, African countries have a poorly banked population, i.e., they do not have a bank account or a credit card.

That is why MPESA, a mobile payment system via SMS, was created years ago. Its users can send and receive money, pay bills and buy products and services through their cell phones. It is an example of how mobile technology can transform financial services and improve financial inclusion.

Payments in North America

It is the continent of credit and cards, which is why their use predominates there, with only Paypal overshadowing cards. Even so, payment services such as Venmo or Cash App, apps that use a prepaid card and a virtual wallet to allow sending or receiving funds between people and businesses, are growing.

An important fact to remember is that US cards do not usually carry 3DS, so they are impossible to authenticate, although we are seeing more and more cards from this country that support it, it is still a minority of the total number of cards.

Payments in Mexico and Central America

How to optimize online payment in one of the most populated countries of the American continent and where cash is the predominant payment method? Using cash.

Although very similar to the process of reloading the wallet in Africa to pay with MPESA, in Mexico they relied on the two largest supermarket networks in the country: OXXO and 7-Eleven.

Basically, the user has to load the wallet at any of the brand’s stores and can then make online purchases. An unbanked method that is increasingly used in Central America.

Payments in Colombia

Just as Bizum was developed in Spain as a payment tool to make it easier for users to send and receive money from their mobile devices, PSE (Secure Online Payment) was developed in Colombia.

It is an online payment system developed by the main financial institutions in Colombia that allows consumers to make online payments through their bank accounts. PSE is one of the most widely used payment methods in Colombia for online purchases and is widely accepted by online merchants and sellers.

Payments in South America

Currently, it is undeniable that PayPal is one of the most widely used online payment platforms in the Americas and also in South America. However, in recent years, a competitor has emerged and is gaining ground: Mercado Pago, Mercado Libre’s payment service. It is similar to OXXO, with the difference that it is exclusive to Mercado Libre users. In addition, it has a wide range of payment options, including bank transfers, credit and debit cards, as well as cash payments at convenience stores and online.

On the other hand, a payment method has emerged in Brazil that is displacing the traditional boleto bancário: PIX. This instant payment system has been adopted by many Brazilian companies and has been widely accepted by consumers. It is a free service, which allows transactions to be made 24 hours a day, 7 days a week, regardless of date or time. In addition, it can be used from any mobile device.

How can alternative payment methods increase hotel bookings?

The first thing a business should do, whether it is a hotel, a travel agency or any company that provides services in the tourism sector, is to analyze the profile of its customersin depth and analyze the type of transactions it receives.

Mainly, each company should analyze its market of travelers to know their tastes and preferences when it comes to making a payment. In this way, the use of one alternative payment method or another can be promoted depending on the country of origin. In addition, the tourist profile has changed and will continue to do so in the coming years, and every year we find more demanding customers, who demand immediacy, personalization and digitization from the tourism sector.

But it is not enough just to offer the payment option at the last step of the purchase or reservation. This must be promoted and must have visibility so that the traveler is more predisposed to make the reservation when they see that they can opt for another method with which they are more familiar and that generates more confidence in making a reservation.

For example, a hotel located in Spain should be prepared to receive the domestic tourist profile and offer payment alternatives such as Bizum. However, it should also adapt to the German public and offer a payment option such as Sofort or to the English public and offer payment initiation. With this you will offer a payment experience tailored to the tastes of your customers, you will increase the conversion of your business and you will be able to reach more customers.

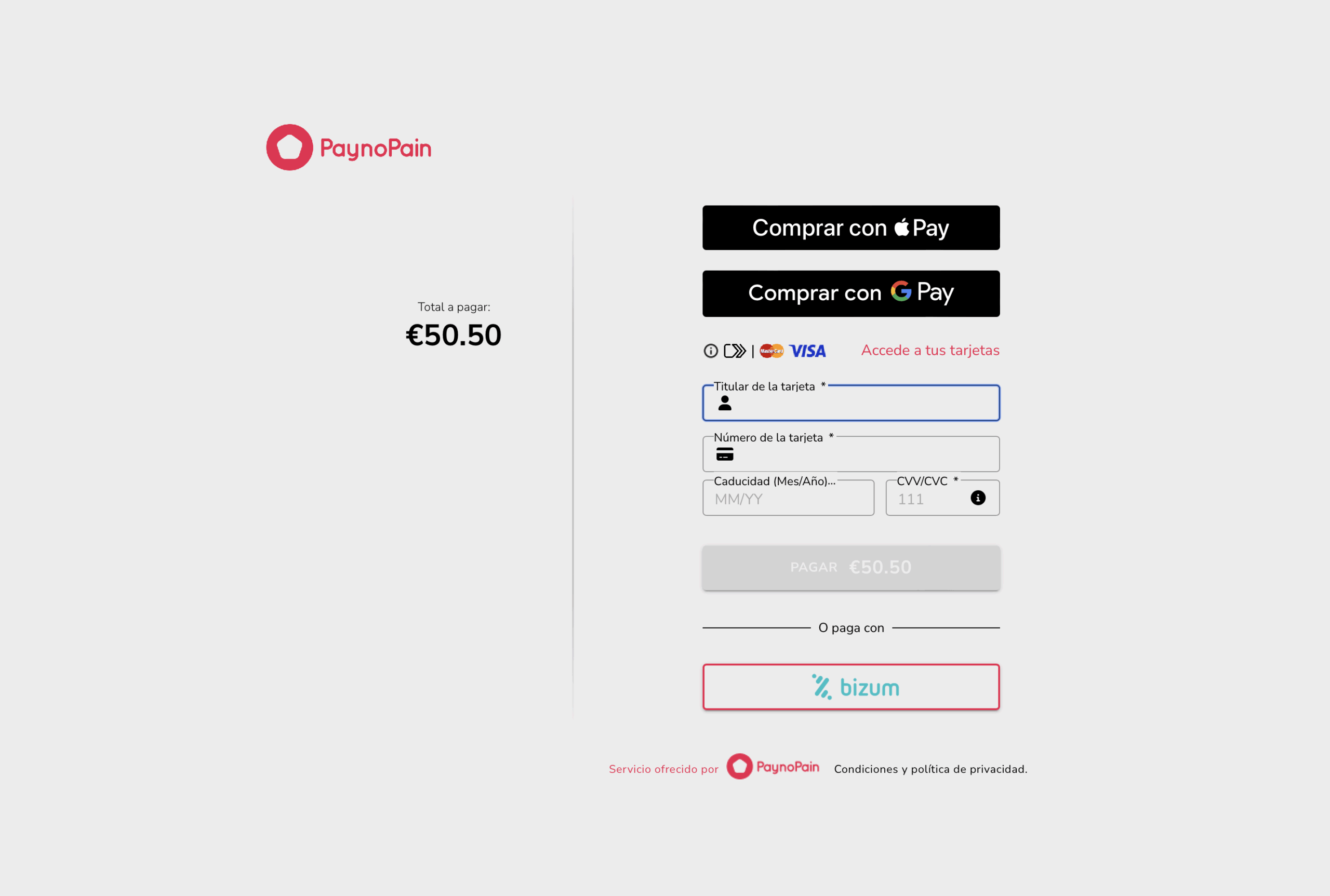

New PaynoPain Checkout

Our new checkout has been designed to simplify the process of deploying and controlling alternative payment methods. In addition, we have developed a feature that allows customization and control of the checkout template, making it easy to adapt to the design of the checkout page.

However, what sets PaynoPain’s MPA apart and makes it even more powerful is that, in addition to offering Checkout with cards and alternative payment methods in a single template, we also allow the integrator to select only the payment method corresponding to the buyer’s language, origin, or country. This way, unnecessary payment options are avoided.

Furthermore, our users of the online payment platform backend can send or generate payment links by selecting a specific payment method.

At PaynoPain, we collaborate with companies that share our vision of innovation, quality, and technological excellence. If you offer complementary solutions or want to distribute our products, together we can go further. We offer you support, training, and real opportunities for joint growth, with global impact.